Academic Institution & Health System-based Cancer Centers: Market Trends and Manufacturer Competitive Assessment

Highlights of the report:

Download a PDF of these Highlights

Against the backdrop of rapid therapeutic innovation, rising treatment complexity, and ongoing reimbursement pressures, Cancer Centers are prioritizing strategies that expand capacity, improve patient access, and support sustainable growth. HIRC's report, Academic Institution & Health System-based Cancer Centers: Market Trends and Manufacturer Competitive Assessment, reviews the market environment and strategic imperatives for Cancer Centers, and provides a competitive assessment of oncology medication manufacturers in Cancer Center engagement. The report addresses the following:

- What are Cancer Centers' top market concerns and strategic priorities in 2026?

- What is the status of Cancer Center activity related to oncology pharmacy and dispensing services (e.g., alternate site infusion, specialty pharmacy)?

- What is the status of oncology preferred drug lists, clinical pathways, and other utilization management tactics?

- What is the status of oncology biosimilar adoption among Cancer Centers?

- Which firms are most often nominated as Cancer Centers' Partner of Choice? Which firms are nominated as providing the best oncology-related support offerings?

- How do pharmaceutical firms benchmark in account engagement and quality of oncology account managers, medical/clinical science liaisons, and field-based reimbursement managers?

Key Finding: Respondents identify Cancer Center facilities expansion as their top strategic imperative in 2026, followed by broadening their contracted payer base to drive patient volume and growth.

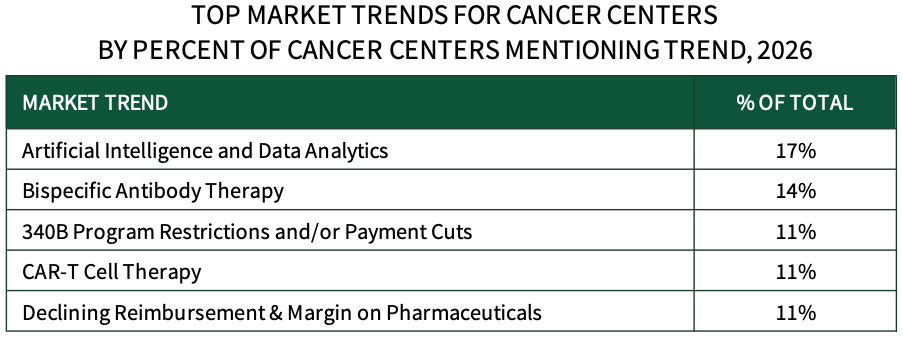

Top Market Trends for Cancer Centers in 2026. The top disruptive market dynamic/trend for Cancer Center senior leadership in 2026 is Artificial Intelligence and Data Analytics, followed by Bispecific Antibody Therapies, 340B Program Restrictions and/or Payment Cuts, CAR-T Cell Therapy, and Declining Reimbursement and Margin on Pharmaceuticals.

The full report provides the complete listing of 50+ trends identified by Cancer Centers, as well as their top strategic imperatives for the next 12-18 months.

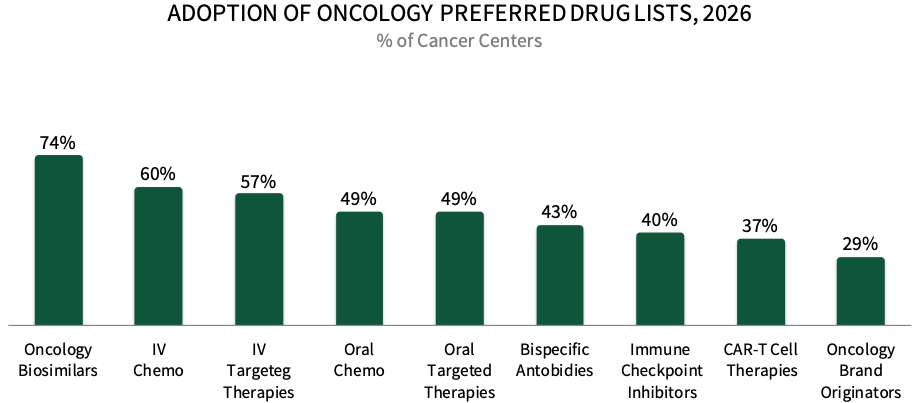

Cancer Centers Most Frequently Designate Preferred Products in Categories with Oncology Biosimilars. About 74% of respondents in HIRC's sample report having preferred oncology biosimilar products in place in 2026, followed by 60% with preferred IV conventional chemotherapy medications, and 57% with preferred IV targeted therapies. The full report examines biosimilars in detail, including which are most preferred, how Cancer Centers promote their use, and which manufacturers offer the best biosimilar support services.

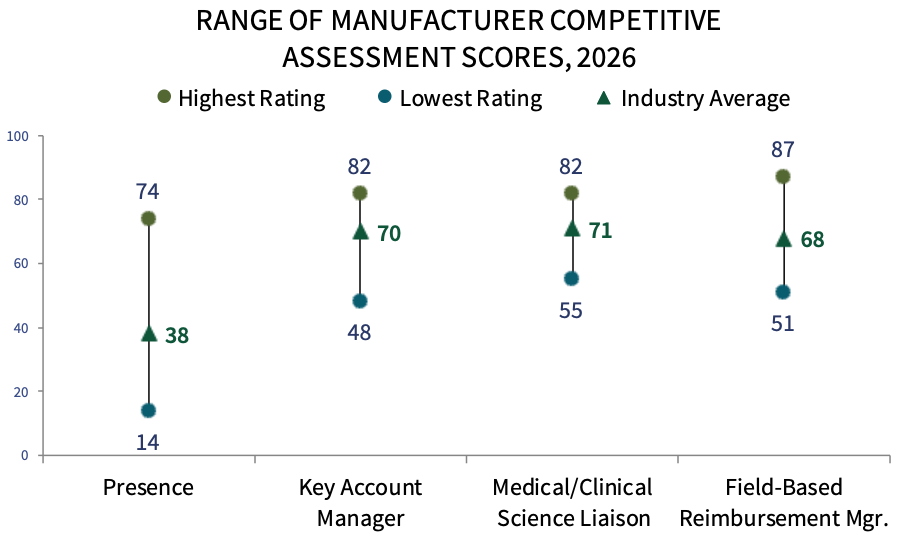

Pharmaceutical Manufacturer Competitive Assessment. Cancer Center respondents were asked to evaluate three types of manufacturer customer-facing personnel as noted below. Pfizer Oncology, AstraZeneca, Genentech, Amgen, and Novartis rate highest in overall manufacturer field personnel engagement in 2026. The complete report provides Cancer Center executives' ratings of 30+ firms active in the oncology space, as well as ratings of manufacturer's oncology-related support offerings and nominations for overall Partner of Choice.

Research Methodology and Report Availability. In January HIRC surveyed 35 executives from Cancer Centers. Online surveys and follow-up telephone interviews were used to gather information. The complete report, Academic Institution & Health System-based Cancer Centers: Market Trends and Manufacturer Competitive Assessment, is available now to HIRC’s Managed Oncology subscribers at www.hirc.com.

Download a PDF of these Highlights

Download Full Report (Subscribers only) >